Note

Go to the end to download the full example code.

9.04 GARCH(1,1) model

We reproduce here the figure 9.5 of the book. Utilitary functions can be found next to this file. Here, we only define codpy-related functions.

Necessary Imports

import os

import sys

import matplotlib.pyplot as plt

import numpy as np

from codpy.kernel import Sampler

try:

CURRENT_DIR = os.path.dirname(os.path.abspath(__file__))

except NameError:

CURRENT_DIR = os.getcwd()

data_path = os.path.join(CURRENT_DIR, "data")

PARENT_DIR = os.path.abspath(os.path.join(CURRENT_DIR, ".."))

sys.path.insert(0, PARENT_DIR)

import utils.ch9.mapping as maps

from utils.ch9.data_utils import stats_df

from utils.ch9.market_data import retrieve_market_data

from utils.ch9.path_generation import generate_paths

from utils.ch9.plot_utils import display_historical_vs_generated_distribution

Parameter definition

def get_cdpres_param():

return {

"rescale_kernel": {"max": 2000, "seed": None},

"rescale": True,

"grid_projection": True,

"reproductibility": False,

"date_format": "%d/%m/%Y",

"begin_date": "01/06/2020",

"end_date": "01/06/2022",

"today_date": "01/06/2022",

"symbols": ["AAPL", "GOOGL", "AMZN"],

}

Get the market data

params = retrieve_market_data()

Defining the map

The GARCH(p,q) map is defined as:

\[\begin{split}\begin{aligned}

X^k &= \mu + \sigma^k \epsilon^k, \\

(\sigma^k)^2 &= \alpha_0 + \sum_{i=1}^{p} \alpha_i (X^{k-i})^2 + \sum_{j=1}^{q} \beta_j (\sigma^{k-j})^2,

\end{aligned}\end{split}\]

where \(\mu \in \mathbb{R}\), \(\{\epsilon^k\}\) is a white noise sequence with unit variance, and \(\sigma^k\) is a stochastic volatility term determined recursively.

The parameters \(\alpha_i\) and \(\beta_i\) denote the GARCH parameters.

q = 1

def garch_pq(x):

import numpy as np

from arch import arch_model

p_values = range(1, 6)

q_values = range(1, 6)

aic_values = np.full((len(p_values), len(q_values)), np.inf)

for i in p_values:

for j in q_values:

try:

model = arch_model(x, vol="Garch", p=i, q=j)

results = model.fit(disp="off") # suppress convergence messages

aic_values[i - 1, j - 1] = results.aic

except:

continue

p, q = np.unravel_index(np.argmin(aic_values, axis=None), aic_values.shape)

print(f"The smallest AIC is {aic_values[p, q]} for model GARCH({p}, {q})")

best_p, best_q = p + 1, q + 1

model = arch_model(x, vol="Garch", p=1, q=1)

results = model.fit()

print(results.summary())

a0 = results.params["omega"]

a = [

results.params[f"alpha[{i+1}]"]

for i in range(best_p)

if f"alpha[{i+1}]" in results.params

]

b = [

results.params[f"beta[{i+1}]"]

for i in range(best_q)

if f"beta[{i+1}]" in results.params

]

return a, b

def estimate_coeff():

asx, bsx = [], []

for i in range(params["data"].values.shape[1]):

ax, bx = garch_pq(params["data"].values[:, i])

asx += [ax]

bsx += [bx]

return np.asarray(asx).T, np.asarray(bsx).T

params["a"], params["b"] = estimate_coeff()

params["q"] = q

params["map"] = maps.composition_map(

[maps.garch_map(), maps.mean_map(), maps.diff(), maps.log_map, maps.remove_time()]

)

params = maps.apply_map(params)

The smallest AIC is 4141.037702885732 for model GARCH(0, 0)

Iteration: 1, Func. Count: 6, Neg. LLF: 16986.629356658286

Iteration: 2, Func. Count: 12, Neg. LLF: 2988.1019261412503

Iteration: 3, Func. Count: 18, Neg. LLF: 2693.0760787188756

Iteration: 4, Func. Count: 24, Neg. LLF: 2100.2759470630394

Iteration: 5, Func. Count: 30, Neg. LLF: 2092.166149373335

Iteration: 6, Func. Count: 36, Neg. LLF: 2102.752613213072

Iteration: 7, Func. Count: 42, Neg. LLF: 2073.109754758848

Iteration: 8, Func. Count: 47, Neg. LLF: 2079.0329137844983

Iteration: 9, Func. Count: 53, Neg. LLF: 2069.501709914081

Iteration: 10, Func. Count: 58, Neg. LLF: 2068.2699961477

Iteration: 11, Func. Count: 63, Neg. LLF: 2067.5250950620048

Iteration: 12, Func. Count: 68, Neg. LLF: 2066.6828346716716

Iteration: 13, Func. Count: 73, Neg. LLF: 2066.542076310764

Iteration: 14, Func. Count: 78, Neg. LLF: 2066.5196720137887

Iteration: 15, Func. Count: 83, Neg. LLF: 2066.5189598207403

Iteration: 16, Func. Count: 88, Neg. LLF: 2066.518854345993

Iteration: 17, Func. Count: 93, Neg. LLF: 2066.518851442866

Iteration: 18, Func. Count: 97, Neg. LLF: 2066.5188514428664

Optimization terminated successfully (Exit mode 0)

Current function value: 2066.518851442866

Iterations: 18

Function evaluations: 97

Gradient evaluations: 18

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -2066.52

Distribution: Normal AIC: 4141.04

Method: Maximum Likelihood BIC: 4157.94

No. Observations: 506

Date: ven., août 22 2025 Df Residuals: 505

Time: 18:42:56 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 125.5477 1.289 97.382 0.000 [1.230e+02,1.281e+02]

Volatility Model

===========================================================================

coef std err t P>|t| 95.0% Conf. Int.

---------------------------------------------------------------------------

omega 3.7144 1.210 3.069 2.149e-03 [ 1.342, 6.087]

alpha[1] 0.9041 9.503e-02 9.514 1.828e-21 [ 0.718, 1.090]

beta[1] 0.0950 9.628e-02 0.987 0.324 [-9.370e-02, 0.284]

===========================================================================

Covariance estimator: robust

The smallest AIC is 3535.7251594871695 for model GARCH(0, 0)

Iteration: 1, Func. Count: 6, Neg. LLF: 602675894.7026879

Iteration: 2, Func. Count: 12, Neg. LLF: 2466.504882261799

Iteration: 3, Func. Count: 19, Neg. LLF: 1923.80528227795

Iteration: 4, Func. Count: 25, Neg. LLF: 1777.3978356491607

Iteration: 5, Func. Count: 30, Neg. LLF: 1770.7938839231458

Iteration: 6, Func. Count: 35, Neg. LLF: 1771.654547784799

Iteration: 7, Func. Count: 41, Neg. LLF: 1765.428021139962

Iteration: 8, Func. Count: 46, Neg. LLF: 1764.8287218853977

Iteration: 9, Func. Count: 51, Neg. LLF: 1764.4434332793412

Iteration: 10, Func. Count: 56, Neg. LLF: 1764.1555080824837

Iteration: 11, Func. Count: 61, Neg. LLF: 1763.8797244685038

Iteration: 12, Func. Count: 66, Neg. LLF: 1763.863264750603

Iteration: 13, Func. Count: 71, Neg. LLF: 1763.8625911283284

Iteration: 14, Func. Count: 76, Neg. LLF: 1763.8625797435848

Iteration: 15, Func. Count: 80, Neg. LLF: 1763.8625797422947

Optimization terminated successfully (Exit mode 0)

Current function value: 1763.8625797435848

Iterations: 15

Function evaluations: 80

Gradient evaluations: 15

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -1763.86

Distribution: Normal AIC: 3535.73

Method: Maximum Likelihood BIC: 3552.63

No. Observations: 506

Date: ven., août 22 2025 Df Residuals: 505

Time: 18:42:57 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 161.9109 0.790 204.905 0.000 [1.604e+02,1.635e+02]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 6.3218 1.499 4.218 2.466e-05 [ 3.384, 9.259]

alpha[1] 0.9650 5.197e-02 18.568 5.800e-77 [ 0.863, 1.067]

beta[1] 0.0350 3.141e-02 1.115 0.265 [-2.654e-02,9.660e-02]

=============================================================================

Covariance estimator: robust

The smallest AIC is 4340.552035447352 for model GARCH(0, 0)

Iteration: 1, Func. Count: 6, Neg. LLF: 16275.618037269702

Iteration: 2, Func. Count: 13, Neg. LLF: 2488.4649454939345

Iteration: 3, Func. Count: 19, Neg. LLF: 2213.4460017426973

Iteration: 4, Func. Count: 25, Neg. LLF: 2263.835511756241

Iteration: 5, Func. Count: 31, Neg. LLF: 2168.8691710334742

Iteration: 6, Func. Count: 36, Neg. LLF: 3108.6099731613394

Iteration: 7, Func. Count: 42, Neg. LLF: 2553.7899311915207

Iteration: 8, Func. Count: 48, Neg. LLF: 21964.18573516304

Iteration: 9, Func. Count: 54, Neg. LLF: 2168.38146506957

Iteration: 10, Func. Count: 60, Neg. LLF: 2166.5913578081636

Iteration: 11, Func. Count: 65, Neg. LLF: 2166.411205000175

Iteration: 12, Func. Count: 70, Neg. LLF: 2166.381080251631

Iteration: 13, Func. Count: 75, Neg. LLF: 2166.3639915405465

Iteration: 14, Func. Count: 80, Neg. LLF: 2166.3019670466983

Iteration: 15, Func. Count: 85, Neg. LLF: 2166.276311352476

Iteration: 16, Func. Count: 90, Neg. LLF: 2166.2760295185026

Iteration: 17, Func. Count: 95, Neg. LLF: 2166.276017723676

Iteration: 18, Func. Count: 99, Neg. LLF: 2166.2760178119124

Optimization terminated successfully (Exit mode 0)

Current function value: 2166.276017723676

Iterations: 18

Function evaluations: 99

Gradient evaluations: 18

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -2166.28

Distribution: Normal AIC: 4340.55

Method: Maximum Likelihood BIC: 4357.46

No. Observations: 506

Date: ven., août 22 2025 Df Residuals: 505

Time: 18:42:57 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 114.6062 0.480 238.672 0.000 [1.137e+02,1.155e+02]

Volatility Model

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

omega 2.7980 0.926 3.023 2.502e-03 [ 0.984, 4.612]

alpha[1] 0.9983 0.149 6.709 1.964e-11 [ 0.707, 1.290]

beta[1] 6.5511e-17 0.134 4.879e-16 1.000 [ -0.263, 0.263]

========================================================================

Covariance estimator: robust

We define our sampler on the mapped data using codpy’s Sampler

You can define your own latent generator function, here we use a simple uniform distribution. But if not provided, a default one will be used by the Sampler class.

mapped_data = params["transform_h"].values

generator = lambda n: np.random.uniform(size=(n, mapped_data.shape[1]))

sampler = Sampler(mapped_data, latent_generator=generator)

params["sampler"] = sampler

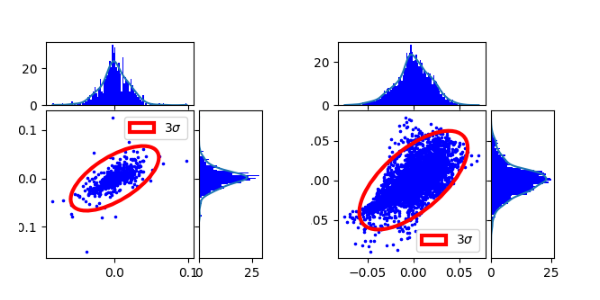

We plot the original distribution vs the generated one

params = display_historical_vs_generated_distribution(params)

params["graphic"](params)

plt.show()

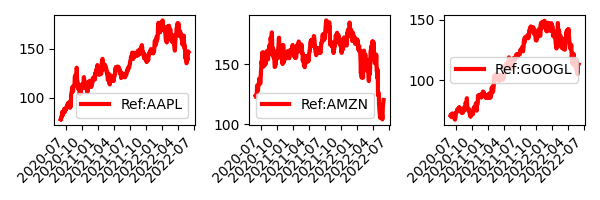

Reproductibility test

We regenerate the same path by generating from the latent representation We make sure we get the original data back.

params["reproductibility"] = True

params = generate_paths(params)

params["graphic"](params)

plt.show()

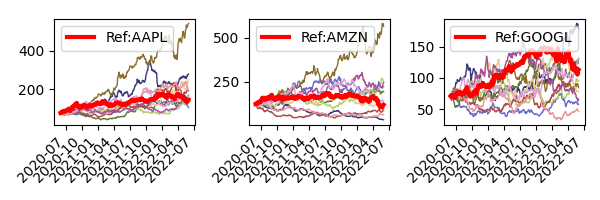

We now generate a new set of 10 paths

params["reproductibility"] = False

params["Nz"] = 10

params = generate_paths(params)

params["graphic"](params)

plt.show()

stats = stats_df(params["transform_h"], params["transform_g"]).T

print(stats)

0 1 2

Mean -6.7e-06(0.00016) -1.2e-06(2.7e-05) -8.4e-06(0.00041)

Variance -0.068(-0.24) -0.44(0.076) -0.089(-0.28)

Skewness 0.0004(0.00039) 0.0005(0.00043) 0.00033(0.00028)

Kurtosis 2(0.31) 6.7(1.1) 1.4(0.6)

KS test 0.54(0.05) 0.64(0.05) 0.72(0.05)

Total running time of the script: (0 minutes 4.835 seconds)