Note

Go to the end to download the full example code.

9.08 Stochastic volatility model

We reproduce here the figure 9.9 of the book. Utilitary functions can be found next to this file. Here, we only define codpy-related functions.

Necessary Imports

import os

import sys

import matplotlib.pyplot as plt

import numpy as np

from codpy.kernel import Sampler

try:

CURRENT_DIR = os.path.dirname(os.path.abspath(__file__))

except NameError:

CURRENT_DIR = os.getcwd()

data_path = os.path.join(CURRENT_DIR, "data")

PARENT_DIR = os.path.abspath(os.path.join(CURRENT_DIR, ".."))

sys.path.insert(0, PARENT_DIR)

import utils.ch9.mapping as maps

from utils.ch9.market_data import retrieve_market_data

from utils.ch9.path_generation import generate_paths

from utils.ch9.plot_utils import display_historical_vs_generated_distribution

Parameter definition

def get_cdpres_param():

return {

"rescale_kernel": {"max": 2000, "seed": None},

"rescale": True,

"grid_projection": True,

"reproductibility": False,

"date_format": "%d/%m/%Y",

"begin_date": "01/06/2020",

"end_date": "01/06/2022",

"today_date": "01/06/2022",

"symbols": ["AAPL", "GOOGL", "AMZN"],

}

Get the market data

params = retrieve_market_data()

Defining the map

This model augments the conditioning model by adding a stochastic volatility term :

\[\begin{split}\begin{split}

\ln X^{k+1} &= \ln X^k + \varepsilon_X^k \mid \sigma^k, \\

\sigma^{k+1} &= \sigma^k + \varepsilon_\sigma^k \mid \sigma^k,

\end{split}\end{split}\]

where \(\varepsilon^k = (\varepsilon_X^k, \varepsilon_\sigma^k)\) are the noise components for the process and volatility, respectively. These are sampled using conditional generators \(G_k^X(\cdot \mid \sigma^k)\) and \(G_k^\sigma(\cdot \mid \sigma^k)\).

params["map"] = maps.composition_map(

(

maps.VarConditioner_map(params),

maps.add_variance_map(var_q=10),

maps.log_map,

maps.remove_time(),

)

)

params = maps.apply_map(params)

We define our sampler on the mapped data using codpy’s Sampler

You can define your own latent generator function, here we use a simple uniform distribution. But if not provided, a default one will be used by the Sampler class.

mapped_data = params["transform_h"].values

generator = lambda n: np.random.uniform(size=(n, mapped_data.shape[1]))

sampler = Sampler(mapped_data, latent_generator=generator)

params["sampler"] = sampler

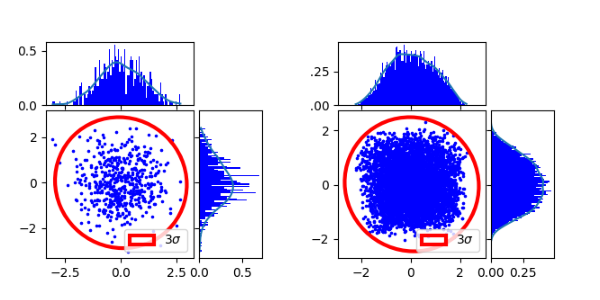

We plot the original distribution vs the generated one

params = display_historical_vs_generated_distribution(params)

params["graphic"](params)

plt.show()

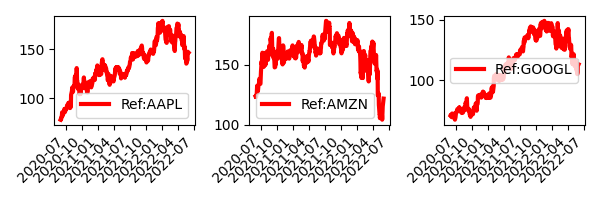

Reproductibility test

We regenerate the same path by generating from the latent representation We make sure we get the original data back.

params["reproductibility"] = True

params = generate_paths(params)

params["graphic"](params)

plt.show()

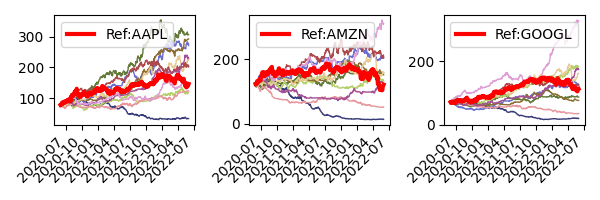

We now generate a new set of 10 paths

params["reproductibility"] = False

params["Nz"] = 10

params = generate_paths(params)

params["graphic"](params)

plt.show()

pass

Total running time of the script: (0 minutes 4.266 seconds)